Direct Reduced Iron (DRI) Market Overview - Definition, scope, and significance

The Direct Reduced Iron (DRI) market encompasses the production and supply of iron reduced directly from iron ore using reducing gases or coal, bypassing the blast furnace route. It serves as a critical feedstock for electric arc furnaces and steelmaking, offering lower carbon emissions and energy consumption. The market scope includes lumps, pellets, and fines, with applications in steel making and construction, and is driven by the shift toward greener metallurgy.

Direct Reduced Iron (DRI) Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

Key drivers include rising demand for low‑carbon steel, stringent environmental regulations, and the growing adoption of electric arc furnace technology. Restraints involve high capital expenditure for gas‑based plants and volatility in natural gas prices. Challenges comprise supply chain disruptions and quality consistency across lumps, pellets, and fines. Opportunities emerge from expanding coal‑based capacity in emerging economies and technological advances that improve reduction efficiency and product uniformity.

Direct Reduced Iron (DRI) Market Growth Trends - Current and emerging trends shaping the market

Current trends show a shift toward gas‑based direct reduction due to lower emissions, while coal‑based routes remain dominant in regions with abundant coal reserves. Pelletized DRI is gaining share because of superior metallurgical properties and handling ease. Digitalization of plant operations, integration of hydrogen as a reducing agent, and strategic partnerships across the value chain are shaping the competitive dynamics and accelerating market growth.

COVID-19 Impact on the Direct Reduced Iron (DRI) Market - Pandemic effects and recovery trajectory

The COVID‑19 pandemic caused temporary plant shutdowns, logistics bottlenecks, and a sharp dip in steel demand, reducing DRI output in 2020. However, the recovery was swift as stimulus packages boosted infrastructure spending and steel consumption rebounded. By 2022 the market regained momentum, and the long‑term outlook remains positive, supported by decarbonization targets that favor DRI over traditional blast furnace iron.

Direct Reduced Iron (DRI) Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape features a mix of integrated steelmakers and technology providers. Major players such as Nucor Corp, Cleveland‑Cliffs Inc., JSW Steel Ltd, and Voestalpine AG operate large‑scale DRI facilities, while SMS Group GmbH, Tenova SpA, and Kobe Steel Ltd supply proprietary reduction technologies. Market consolidation is evident through joint ventures and capacity expansions aimed at securing raw material access and reducing production costs.

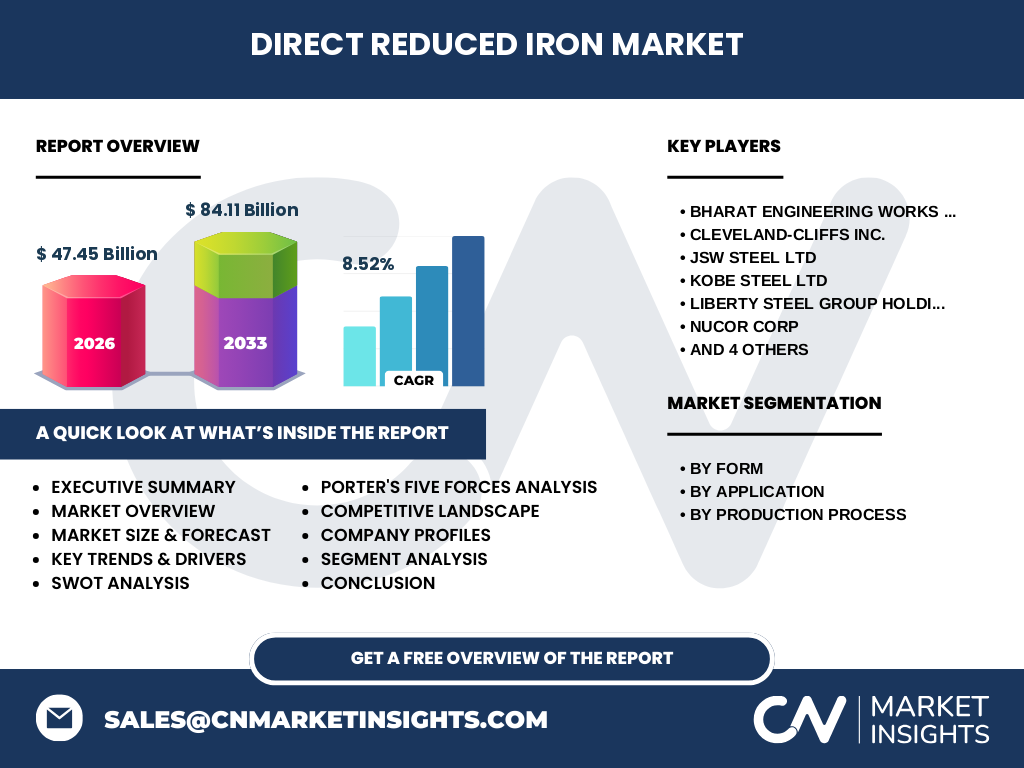

Executive Summary - High-level overview and key findings about Direct Reduced Iron (DRI) Market

The executive summary highlights that the Direct Reduced Iron market was valued at 47.45 Billion in 2026 and is projected to reach 84.11 Billion by 2033, growing at a CAGR of 8.52 %. Growth is fueled by increasing steel demand, environmental policies, and the rise of electric arc furnace steelmaking. The report segments the market by form, application, and production process, and profiles ten leading companies driving innovation and capacity additions.

Direct Reduced Iron (DRI) Market Forecast - Projections for 2025-2032 period

Market forecast models indicate robust expansion from 2027 through 2033, with the valuation climbing from 47.45 Billion in 2026 to 84.11 Billion by 2033, reflecting an 8.52 % CAGR. The forecast assumes continued adoption of gas‑based reduction, higher pellet penetration, and supportive policy frameworks in major steel‑producing regions. Sensitivity analysis shows upside potential if hydrogen‑based reduction scales commercially.

Direct Reduced Iron (DRI) Market Size and Share by Segmentation - Breakdown by {segmentData}

Segmentation analysis breaks the market into three form categories – lumps, pellets, and fines – with pellets commanding the largest share due to superior metallurgical performance. By application, steel making and construction dominate demand, accounting for the bulk of consumption. Production process splits between coal‑based and gas‑based routes, where gas‑based is growing faster owing to lower carbon intensity, while coal‑based retains a strong base in cost‑sensitive markets.

Global Direct Reduced Iron (DRI) Market Size and Share by Region - Geographic distribution

Global market size distribution shows that Asia‑Pacific leads in volume owing to massive steel output in China and India, followed by the Middle East where gas‑based plants are prevalent. Europe and North America contribute significant value through advanced technology adoption and stringent emission standards. The report provides a detailed regional breakdown, highlighting growth rates and investment hotspots for each geography.

Regional Analysis of the Direct Reduced Iron (DRI) Market - Detailed regional market performance

Regional analysis reveals that the Middle East benefits from abundant natural gas, enabling low‑cost gas‑based DRI production, while India expands coal‑based capacity to meet domestic steel demand. China’s policy push for ultra‑low emissions accelerates pellet adoption. Latin America shows emerging interest in hybrid coal‑gas plants. Each region’s regulatory environment, raw material availability, and infrastructure shape distinct competitive dynamics and investment attractiveness.

Leading Company Profiles in the Direct Reduced Iron (DRI) Market - Industry players and strategies

Leading company profiles cover ten key players: Bharat Engineering Works Pvt Ltd, Cleveland‑Cliffs Inc., JSW Steel Ltd, Kobe Steel Ltd, Liberty Steel Group Holdings UK Ltd, Nucor Corp, SMS Group GmbH, Tenova SpA, Ternium SA, and Voestalpine AG. These firms drive capacity expansions, technology licensing, and strategic alliances. Their product portfolios span lumps, pellets, and fines, and they invest heavily in hydrogen‑ready reduction pathways to future‑proof operations.

Porter's Five Forces Analysis of the Direct Reduced Iron (DRI) Market - Competitive forces assessment

Porter’s Five Forces assessment indicates moderate threat of new entrants due to high capital intensity and technology barriers. Supplier power is elevated for natural gas and high‑grade iron ore, while buyer power grows as steelmakers diversify sourcing. Substitute threat remains low because DRI offers unique metallurgical advantages over scrap. Competitive rivalry is intense among integrated producers and technology vendors, prompting continuous innovation and cost optimization.

SWOT Analysis of the Direct Reduced Iron (DRI) Market - Strengths, weaknesses, opportunities, threats

SWOT analysis highlights strengths such as lower CO₂ emissions versus blast furnace iron, flexibility in feedstock, and compatibility with electric arc furnaces. Weaknesses include high upfront capital, sensitivity to gas price swings, and quality variability in fines. Opportunities lie in hydrogen‑based reduction, expanding pellet markets, and policy incentives for green steel. Threats encompass regulatory uncertainty, raw material supply disruptions, and competition from scrap‑based steelmaking.

Direct Reduced Iron (DRI) Market Value Chain Analysis - Industry structure and value flow

Value chain analysis traces raw material extraction, iron ore preparation, reduction (coal‑based or gas‑based), product finishing into lumps, pellets, or fines, and downstream delivery to electric arc furnace steelmakers and construction firms. Midstream players such as SMS Group GmbH and Tenova SpA provide reactor technology and engineering services, while integrated steelmakers like Nucor Corp and JSW Steel Ltd control both production and end‑use, creating vertical integration advantages.

Key Investment Insights in the Direct Reduced Iron (DRI) Market - Strategic investment recommendations

Key investment insights recommend prioritizing gas‑based and hydrogen‑ready DRI projects in regions with cheap natural gas and supportive carbon pricing. Investing in pelletizing capacity enhances product value and meets premium steelmaker specifications. Strategic partnerships with technology providers such as Tenova SpA and SMS Group GmbH reduce execution risk. Monitoring policy shifts in major economies will identify timing for capacity additions and potential subsidy capture.

Direct Reduced Iron (DRI) Market Conclusion - Summary and key takeaways

The conclusion underscores that the Direct Reduced Iron market is on a strong growth trajectory, driven by decarbonization imperatives and the rise of electric arc furnace steelmaking. With a 2026 valuation of 47.45 Billion and a 2033 forecast of 84.11 Billion at 8.52 % CAGR, stakeholders should focus on technology upgrades, pellet expansion, and regional diversification to capture emerging demand and mitigate raw material volatility.

Research Methodology - How this research was conducted

Research methodology combines primary interviews with industry executives, plant operators, and technology suppliers, complemented by secondary data from trade associations, government publications, and financial filings. Quantitative modeling uses bottom‑up capacity tracking and top‑down demand forecasting, calibrated to the 2026 market size of 47.45 Billion. Scenario analysis incorporates policy, energy price, and technology adoption variables to generate the 2027‑2033 forecast of 84.11 Billion at 8.52 % CAGR.

Research Scope - Coverage and limitations

Research scope covers the global Direct Reduced Iron market across all major forms – lumps, pellets, fines – applications in steel making and construction, and production processes both coal‑based and gas‑based. The study period spans 2026 as base year with forecasts through 2033. Geographic coverage includes Asia‑Pacific, Middle East, Europe, North America, and Latin America. Limitations acknowledge reliance on publicly disclosed capacity data and the exclusion of niche specialty grades.

Key Companies and Recent Developments in the Direct Reduced Iron (DRI) Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

Key companies and recent developments feature Bharat Engineering Works Pvt Ltd expanding its coal‑based DRI line, Cleveland‑Cliffs Inc. announcing a new gas‑based plant in the Midwest, JSW Steel Ltd commissioning a pelletizing unit, Kobe Steel Ltd launching a hydrogen‑ready reduction pilot, Liberty Steel Group Holdings UK Ltd securing a long‑term gas supply contract, Nucor Corp investing in advanced furnace integration, SMS Group GmbH releasing a next‑generation reactor, Tenova SpA forming a joint venture for green DRI, Ternium SA upgrading its pellet capacity, and Voestalpine AG publishing a decarbonization roadmap.